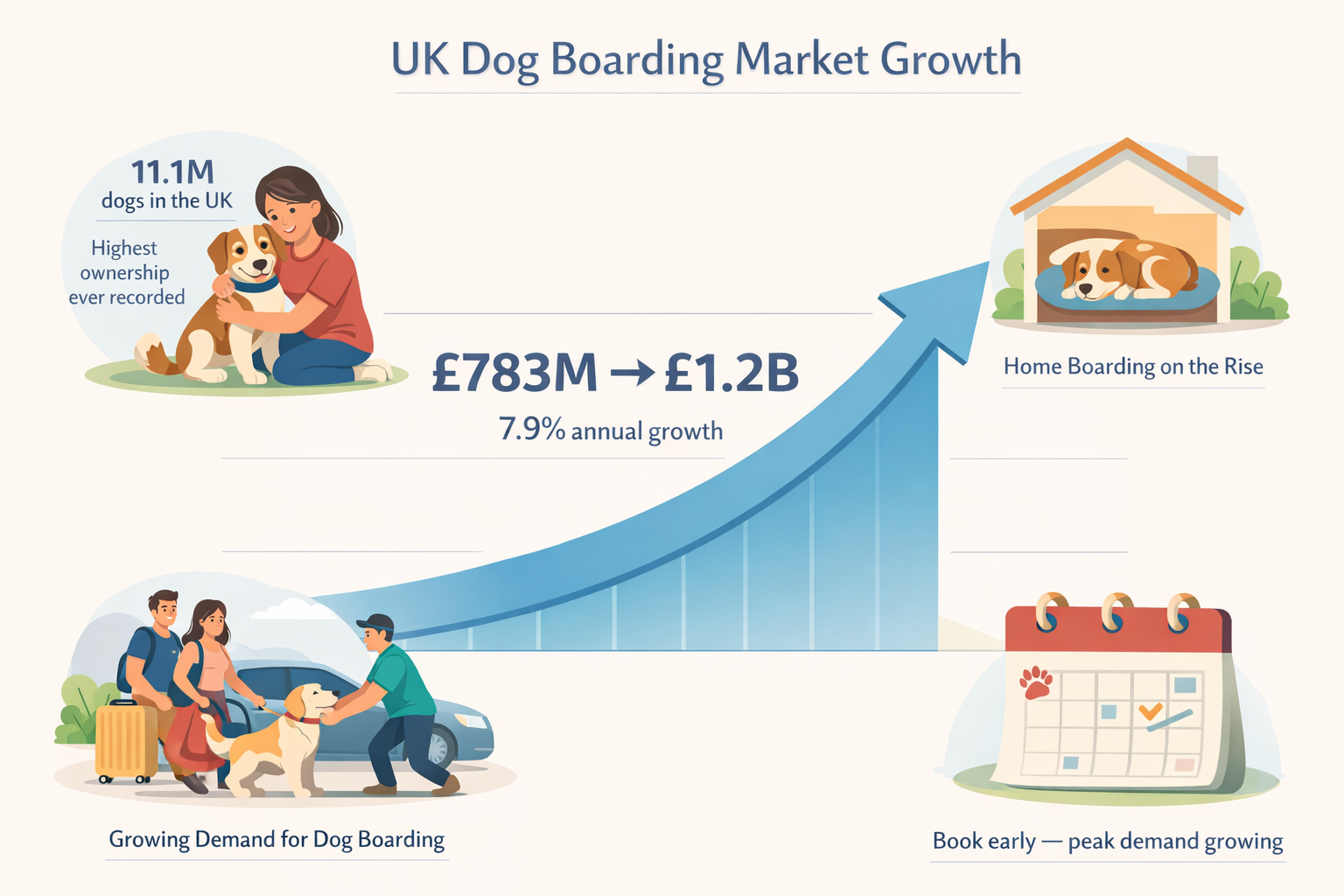

The UK dog boarding market reached £783.2 million in 2024 according to Grand View Research, with projections showing it could hit £1.2 billion by 2030. Yet beneath those numbers lies a paradox: while demand soars, licensed boarding kennels are actually declining — down 27% between 2023–2024 according to The Pet Industry Federation.

Key Findings

- 7.9% compound annual growth rate projected through 2030 (Grand View Research)

- Dogs account for the vast majority of boarding market revenue

- Licensed home boarders grew 22.5% in a single year (2017–2018), while traditional kennels declined sharply

- 11.1 million dogs in the UK — the highest population ever recorded (PDSA PAW Report 2025)

- The UK represents roughly a tenth of the global pet boarding market

Methodology Note

Market valuation data comes from Grand View Research's analysis of commercial boarding services. Pet ownership figures are sourced from the PDSA PAW Report 2025. Licensing data is from The Pet Industry Federation and industry reporting on local authority figures. Statistics may not capture unlicensed boarding activity or all small-scale operators.

Market Size and Growth

The 7.9% annual growth rate puts pet boarding comfortably ahead of most traditional service industries. That rate reflects not just more dogs needing care, but owners spending more per stay — premium options including enrichment activities, webcam access, and luxury accommodation are capturing a growing slice of the market.

| Metric | Figure | Source |

|---|---|---|

| 2024 market value | £783.2 million | Grand View Research |

| 2030 projected value | £1,214.9 million | Grand View Research |

| Annual growth rate (CAGR) | 7.9% | Grand View Research |

| UK share of global market | ~9% | Grand View Research |

The Kennel Decline vs Home Boarding Rise

This is the most striking trend in the data. Traditional kennels are closing — down 27% between 2023–2024 according to The Pet Industry Federation — while home boarding continues to grow. Licensed home boarders jumped from 4,814 to 5,841 operators between 2017–2018 alone, a 22.5% increase in a single year.

The reasons are largely economic. Kennels face rising energy costs (heating and ventilation run year-round), increasing licensing fees, staffing difficulties, and regulatory compliance expenses. Home boarders operate with far lower overheads — no purpose-built facility to maintain, no commercial energy bills, fewer staff.

For pet owners, this shift has practical implications. There are fewer kennel options in many areas than there were five years ago, meaning earlier booking is essential during peak periods. On the other hand, home boarding availability has expanded, offering more personalised care — often at comparable prices.

What's Driving Demand

According to the PDSA PAW Report 2025, the UK now houses 11.1 million dogs and 10.5 million cats — the highest dog population ever recorded. Dog ownership has climbed steadily over the past decade, with the pandemic accelerating the trend.

The COVID-19 pandemic accelerated pet adoption, and many of those new owners are now returning to offices and booking holidays, creating sustained boarding demand. Consumer spending on pet services continues to rise, driven by treating pets as family members who deserve professional care rather than a favour from a neighbour.

Holiday booking patterns show strong seasonal peaks during school holidays and Christmas. Many facilities report consistent demand year-round, with waiting lists common during peak periods.

Regional Patterns

London has the highest concentration of boarding facilities, reflecting both population density and the number of dog owners who travel frequently for work. The capital's mix of business travellers and families creates year-round demand that supports a large number of providers.

Yorkshire stands out as a boarding hotspot. Leeds and York both rank among the top UK cities for boarding availability — likely driven by the region's large dog-owning population combined with strong tourism creating consistent demand.

Urban areas generally show higher facility density but smaller operations, while rural regions tend toward fewer, larger-capacity kennels that often bundle boarding with other pet services like grooming and daycare. Wales concentrates provision around Swansea and Cardiff, while Scotland's provision clusters around Edinburgh and Glasgow.

What This Means Going Forward

The growth projections remain optimistic despite facility closures. Demand fundamentals are strong — more dogs, more travel, more willingness to spend on quality care. The market is shifting rather than shrinking.

For pet owners, the practical takeaway: book early, especially for school holidays and Christmas. The combination of growing demand and declining kennel numbers means availability will only tighten. Home boarding is increasingly where the capacity is, and it's worth exploring if you haven't already.

For the industry, home boarding's lower cost base makes it the natural growth area. Technology — booking platforms, monitoring systems, communication tools — is becoming a standard expectation rather than a nice-to-have, and operators who adopt early will have an edge.

Frequently Asked Questions

How big is the UK dog boarding market?

Grand View Research values the UK pet boarding market at £783.2 million in 2024, with dogs representing the vast majority of revenue. The market is projected to grow at 7.9% annually, reaching over £1.2 billion by 2030.

Why are boarding kennels closing despite rising demand?

Traditional kennels face rising operational costs — energy, staffing, licensing fees, and regulatory compliance — that are squeezing margins. The Pet Industry Federation reports a 27% decline in licensed kennels between 2023–2024. Many operators are shifting to home boarding models with lower overheads.

Is home boarding replacing traditional kennels?

Partially. Home boarding is the fastest-growing segment, with licensed operators increasing 22.5% between 2017–2018. It offers lower costs for operators and more personalised care for dogs, but traditional kennels still serve owners who need structured, facility-based care — particularly for multiple dogs or those with specific needs.

How many dogs are there in the UK?

The PDSA PAW Report 2025 puts the UK dog population at 11.1 million — the highest ever recorded. Cat ownership stands at 10.5 million, while the rabbit population has declined to around 700,000.